Debt settlement can help you reduce your outstanding unsecured debt, but choosing the right company is crucial. This guide evaluates leading debt settlement providers in 2025, focusing on fees, customer satisfaction, and eligibility criteria to help you make an informed decision. Here’s what you need to know:

- Freedom Debt Relief: Requires $7,500 minimum debt. Fees range from 15–25% of enrolled debt. Offers a refund guarantee if total costs exceed original debt.

- National Debt Relief: $7,500 minimum debt. Transparent performance-based fees (15–25%). Highly rated for customer satisfaction and compliance.

- Accredited Debt Relief: $10,000 minimum debt for settlement. Offers alternative solutions for smaller debts starting at $2,500.

- Pacific Debt Relief: $10,000 minimum debt. Fees around 25%, calculated on settled debt. No upfront fees.

- Optimal Debt Solutions: No strict minimum debt requirement. Works with various unsecured debts. Strong BBB rating and regulatory compliance.

- New Era Debt Solutions: No upfront fees. Fees range from 14–25%. High customer satisfaction with transparent policies.

- Americor Debt Relief: $10,000 minimum debt. A+ BBB rating but has faced regulatory scrutiny.

Quick Comparison

| Company | Minimum Debt | Fees | Customer Rating | Key Feature |

|---|---|---|---|---|

| Freedom Debt Relief | $7,500 | 15–25% (enrolled) | Mixed | Refund guarantee for excess costs |

| National Debt Relief | $7,500 | 15–25% (enrolled) | High | Strong compliance and transparency |

| Accredited Debt Relief | $10,000 | 15–25% (enrolled) | Good | Alternative options for smaller debts |

| Pacific Debt Relief | $10,000 | ~25% (settled) | Good | No upfront fees |

| Optimal Debt Solutions | None | Varies | High | No strict debt minimum |

| New Era Debt Solutions | None | 14–25% (enrolled) | High | Transparent, performance-based fees |

| Americor Debt Relief | $10,000 | Varies | Good | Strong BBB rating, past scrutiny |

When considering debt settlement, factor in fees, program duration, and potential credit impact. Always verify the company’s licensing and read contracts thoroughly before enrolling.

Pros and Cons of Debt Relief and Settlement

1. Freedom Debt Relief

Freedom Debt Relief is a prominent U.S.-based company specializing in negotiating reduced payoffs for unsecured debts.

Regulatory History

Freedom Debt Relief has faced regulatory scrutiny, resulting in notable settlements that highlight the need to thoroughly understand its program terms. In July 2019, the Consumer Financial Protection Bureau (CFPB) reached a settlement with the company, which included $20 million in customer restitution and a $5 million civil penalty. The CFPB alleged:

"The Bureau's lawsuit alleged that Freedom Debt Relief violated the Telemarketing Sales Rule by charging advance fees and failing to inform consumers of their rights to funds they deposited with the company. The Bureau also alleged that Freedom Debt Relief violated the Consumer Financial Protection Act of 2010 by charging consumers without settling their debts as promised, charging consumers after having them negotiate their own settlements with creditors, and misleading consumers about the company's fees and its ability to negotiate directly with all of a consumer's creditors."

– Consumer Financial Protection Bureau, 2019

Additionally, in 2023, the company agreed to a $9.75 million settlement for a class-action lawsuit related to alleged violations of the Telephone Consumer Protection Act. While Freedom Debt Relief did not admit any wrongdoing, these cases emphasize the importance of reviewing program details and understanding the associated risks.

Fee Structures

Freedom Debt Relief employs a performance-based fee structure, meaning fees are only charged after a debt settlement is successfully negotiated and approved by the customer. The key fees include:

- A settlement fee ranging from 15–25% of the original enrolled debt

- A one-time account setup fee of $9.95

- A $9.95 monthly maintenance fee for the escrow account

For example, if a $15,000 debt is reduced to an $8,000 settlement, a 25% fee would amount to $3,750, based on the original enrolled debt. It's also worth noting that any forgiven debt could be considered taxable unless you are insolvent at the time of settlement.

Minimum Debt Requirements

Freedom Debt Relief requires a minimum of $7,500 in unsecured debt to enroll in its program. Eligible debts typically include credit cards, personal loans, and medical bills. However, secured debts like mortgages or auto loans, as well as federal student loans, do not qualify.

Here’s a quick comparison of minimum debt requirements across similar companies:

| Company | Minimum Debt Required | Service Type |

|---|---|---|

| Freedom Debt Relief | $7,500 | Debt Settlement |

| National Debt Relief | $10,000 | Debt Settlement |

| Accredited Debt Relief | $10,000 | Debt Settlement |

| Pacific Debt Relief | $10,000 | Debt Settlement |

Program Duration

Debt settlement programs often take several years to complete. During this time, interest and fees on your debts may continue to accumulate if negotiations take longer than expected, potentially increasing the total amount owed. Understanding the timeline is crucial to managing expectations and avoiding surprises.

Customer Satisfaction

Freedom Debt Relief offers a unique Program Guarantee, promising a full refund if the total settlement amount, including fees, exceeds the original enrolled debt. This guarantee is uncommon in the debt relief industry and addresses concerns about fee transparency and prolonged timelines.

However, customer feedback often highlights challenges such as the impact on credit scores and the lengthy settlement process. Creditors may delay negotiations until accounts are significantly overdue, which can further affect credit. While Freedom Debt Relief has built strong relationships with major creditors due to its extensive experience, customers are advised to carefully review all terms and maintain realistic expectations regarding the program's timeline and potential credit impact.

2. National Debt Relief

National Debt Relief stands out for its commitment to transparency and customer protection. With strong industry credentials and a fee structure that prioritizes client success, the company has built a reputation for trustworthiness and effective debt solutions.

Accreditation and Compliance

National Debt Relief is accredited by key industry organizations, reinforcing its credibility. It holds an A+ rating from the Better Business Bureau of New York, Platinum Accreditation from the International Association of Professional Debt Arbitrators (IAPDA), and membership with the American Association for Debt Resolution (AADR). These certifications are not just badges - they represent ongoing audits and compliance with industry standards. Few companies in the debt relief industry can claim accreditation from all three of these major organizations.

This dedication to compliance hasn’t gone unnoticed. Forbes Advisor has named National Debt Relief the "Best Debt Relief and Settlement Companies of 2025" for three years running. It also earned recognition for its fee transparency, receiving a 4.5 out of 5-star rating.

"It's a true privilege to once again be named the Best Debt Relief Company by a respected authority like Forbes Advisor, known for guiding consumers toward smart financial choices. This continued recognition for National Debt Relief shows how committed our team is to being transparent, putting clients first and delivering real results." – Alex Kleyner, Chief Executive Officer and Co-Founder, National Debt Relief

Let’s take a closer look at how this commitment to compliance translates into its fee structure.

Fee Structures

National Debt Relief employs a performance-based fee model that ensures clients only pay for results. There are no upfront costs, and fees range from 15–25% of the enrolled debt, depending on the state and debt amount. Importantly, fees are only charged when three conditions are met: a settlement offer is received from the creditor, the client approves the settlement, and at least one payment toward the settlement is made.

"At National Debt Relief we do not earn anything unless we get you results. Specifically, 3 things must happen for a fee to be earned for the service. First, a settlement offer must be received from the creditor, we must receive your approval of the settlement, and finally at least 1 settlement payment to the creditor must be made. Only then would our fee be earned and charged to your Dedicated Account." – National Debt Relief

All fees are included in a monthly program payment, which is deposited into an FDIC-insured dedicated account. On average, clients can save about 50% of their total debt before fees, or 30% after fees.

Minimum Debt Requirements

To qualify for National Debt Relief’s program, clients need a minimum of $7,500 in unsecured debt. The program covers a wide range of unsecured debts, such as credit cards, personal loans, medical bills, collections, repossessions, business debts, and some private student loans. However, secured debts like mortgages or auto loans, as well as past-due taxes and federal student loans, are typically excluded.

Customer Satisfaction

National Debt Relief has earned high praise from its clients, reflecting both its transparent practices and effective results. It holds a 4.8 out of 5 rating on Trustpilot from 31,949 reviews and a 4.83 out of 5 rating on ConsumerAffairs from 46,954 reviews. This success is driven by its "Whole Human Finance™" approach, which addresses not only financial challenges but also the emotional and behavioral aspects of debt. The company’s efforts have also earned it top rankings from platforms like TopConsumerReviews, TopTenReviews, and ConsumersAdvocate.

"When a client comes to us, their debt isn't just hurting their wallet, it's impacting their whole life and entire sense of self. Our program not only focuses on helping someone out of debt, but we also help them tackle the psychological, behavioral and emotional aspects of their relationship with money, with the goal that when they graduate, they never need debt relief again." – Natalia Brown, Chief Compliance and Consumer Affairs Officer, National Debt Relief

3. Accredited Debt Relief

Accredited Debt Relief focuses on helping clients with larger debts while also offering options for those with smaller financial obligations. The company follows a specific approach to debt settlement, setting itself apart from other debt relief providers. Let’s take a closer look at their debt thresholds and the alternatives they provide.

Minimum Debt Requirements

To qualify for Accredited Debt Relief's debt settlement programs, clients need to have at least $10,000 in unsecured debt. This requirement highlights the company's expertise in handling larger debt cases, often working with clients who owe $30,000 or more. However, for individuals who don’t meet the $10,000 minimum, the company connects them to alternative solutions through its provider network, such as debt consolidation loans, credit counseling, and debt management plans. These options are available to those with unsecured debts starting at $2,500.

This tiered structure allows Accredited Debt Relief to cater to a wide range of clients. By focusing on larger, more complex cases while offering accessible alternatives for smaller debts, the company ensures that clients with varying financial challenges can find a suitable path forward.

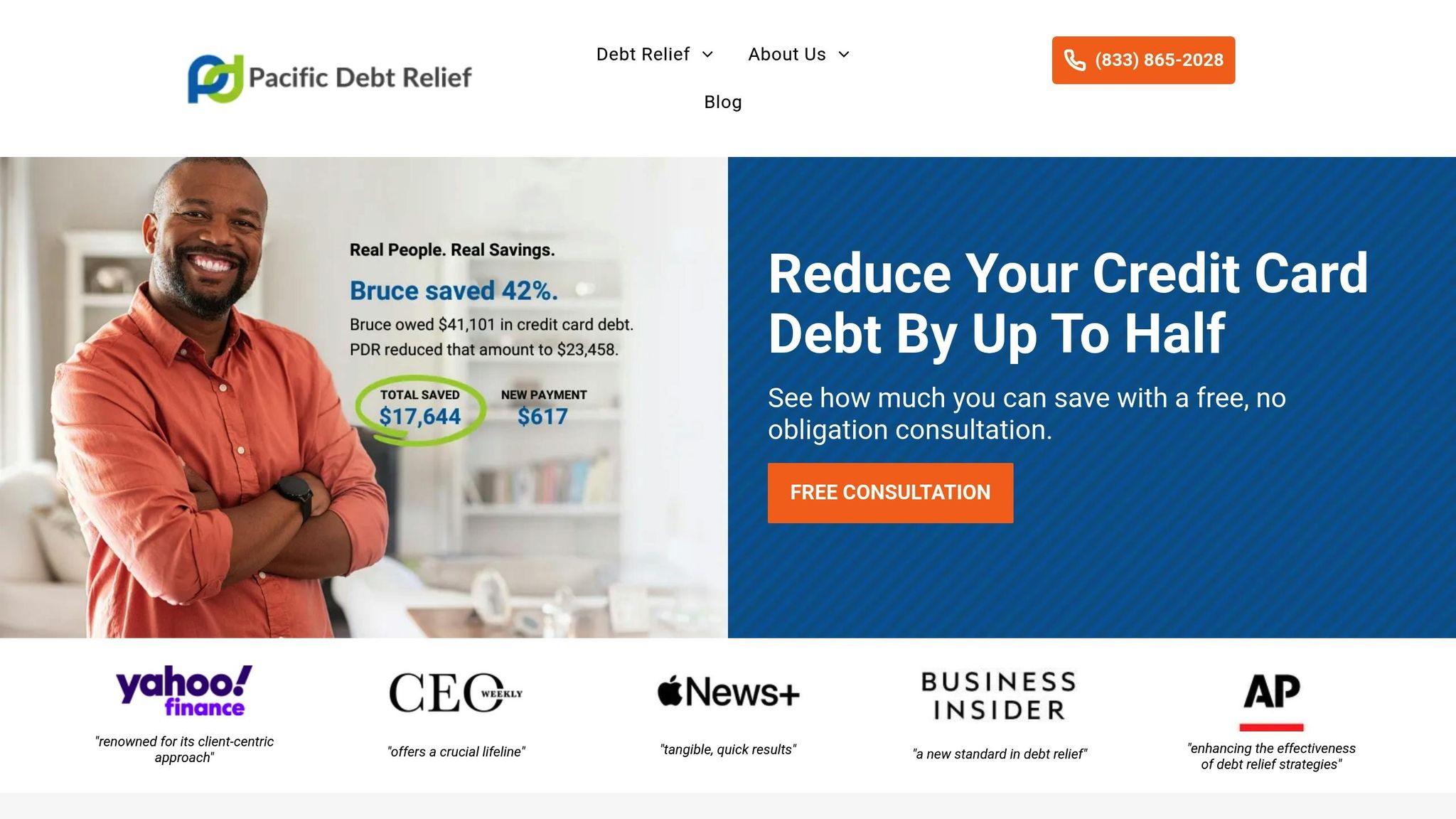

4. Pacific Debt Relief

Pacific Debt Relief focuses on helping clients with unsecured debts starting at $10,000. This means they primarily work with individuals facing significant financial challenges, often involving multiple creditors and intricate debt situations. Their approach is built around a performance-based fee structure, which is explained in more detail below.

Fee Structures

Pacific Debt Relief follows a performance-based fee model, adhering to strict regulatory guidelines. Under this model, clients are only charged after the company successfully negotiates and settles their debts - no upfront fees are required, fully aligning with Federal Trade Commission (FTC) rules.

"Pacific Debt is in full compliance with the new FTC rules. What this means to you is that we do not charge any upfront fees, you must authorize all settlements and PDI does not get paid until you see results."

Settlement fees generally range between 15% and 25% of the enrolled debt, with the average fee landing around 25%. Importantly, these fees are calculated based on the settled debt amount rather than the original balance, which can be advantageous for clients when significant reductions are achieved.

While the fee structure falls within industry norms, the average fee is on the higher end of the spectrum. Clients are required to make monthly payments into an FDIC-insured escrow account. The typical setup fees for these accounts are about $8–$10, with ongoing monthly fees averaging around $10.

"Fees are on the higher end. Debt relief fees range from 15% to 25% of the debt you enroll, and Pacific Debt Relief charges average fees of around 25%. That's within the usual range, but on the higher side."

To get specific pricing details, clients must go through a consultation, as the company does not disclose pricing information online or over the phone without this step. This can make it harder to compare their fees with other options.

"You can't find any information about pricing online, and representatives won't provide exact numbers on the phone until you go through a free consultation. This makes it harder to compare other options."

sbb-itb-3a8c5bf

5. Optimal Debt Solutions

Optimal Debt Solutions specializes in helping clients manage unsecured debt by working directly with creditors to negotiate lower balances.

Accreditation and Compliance

The company maintains an A+ rating with the Better Business Bureau (BBB) and is accredited by the Association for Consumer Debt Relief (ACDR/AACR). This reflects its dedication to ethical practices and adherence to strict regulatory guidelines. Additionally, F10 Financial Group, LLC, operating as Optimal Debt Solutions, is officially registered with the California Department of Financial Protection and Innovation (DFPI) under Registration Number 01-CCFPL-2095431-346645. Impressively, the company has no recorded complaints with the Federal Trade Commission (FTC) or the Consumer Financial Protection Bureau (CFPB).

This solid regulatory foundation allows the company to offer flexible program options tailored to clients' needs.

Minimum Debt Requirements

Optimal Debt Solutions stands out by not imposing a strict minimum debt requirement, making its services accessible to a broader range of clients. Its programs are designed for individuals struggling to keep up with payments on unsecured debts such as personal loans, credit cards (including retail cards), medical bills, collection accounts, and payday loans. Generally, accounts must be at least 90 days overdue to qualify for creditor negotiations, and participants must reside in an eligible state. This program is ideal for those facing mounting debt, high-interest rates, and limited financial resources.

6. New Era Debt Solutions

New Era Debt Solutions has carved out a niche in the debt relief industry with its commitment to regulatory compliance and a transparent, performance-based fee model aimed at helping clients navigate financial challenges.

Fee Structures

New Era Debt Solutions operates on a performance-based fee model, fully compliant with Federal Trade Commission (FTC) regulations. This means clients are charged fees only after a successful settlement is reached. Rates typically range from 14% to 23%, though some sources suggest a slightly broader range of 15% to 25%.

"No debt settlement company should charge you any fees at all unless or until your debt is settled. Performance-based fees have always been the best model for the consumer. Recently, the Federal Trade Commission (FTC) made it law and as of October 27, 2010, anything besides paying for performance is simply illegal. Fees can only be collected after a settlement has been made and approved by the client."

– New Era Debt Solutions

These fees are usually based on the initial enrolled debt amount. However, some reviewers have noted that the company could improve clarity around how fees are calculated.

Clients are also required to deposit funds into an FDIC-insured escrow account, which comes with a monthly service fee of $18.95 - higher than the industry average of around $10.

Minimum Debt Requirements

New Era Debt Solutions provides assistance for a wide range of unsecured debts, such as credit card balances, personal loans, medical bills, and collection accounts. The company does not publicly disclose a strict minimum debt requirement, which could make its services more accessible to individuals with varying levels of debt.

Customer Satisfaction

The company’s focus on performance-based fees and adherence to FTC rules has earned it praise from many clients. However, concerns about fee transparency have been highlighted. Bankrate noted:

"New Era Debt Solutions is not transparent about its fees. While it makes it clear that there are no upfront fees and it uses a 'performance-based' fee model, the company does not reveal a free range like many of its competitors do."

– Bankrate

Despite these concerns, many clients value the assurance that fees are only charged after successful settlements. This approach, combined with regulatory compliance, positions New Era Debt Solutions as a trusted option in the debt settlement industry.

7. Americor Debt Relief

Next up in our review is Americor Debt Relief, a company that has carved out a notable place in the debt relief industry. Known for its strong regulatory adherence and consistent client outcomes, Americor has built a reputation for reliability and compliance.

Accreditation and Compliance

Americor Debt Relief has been a BBB Accredited Business since November 17, 2015, and holds an impressive A+ rating from the Better Business Bureau. This rating reflects the company’s commitment to the BBB Standards for Trust. To ensure ongoing compliance, Americor employs a dedicated team that oversees regulations, maintains licensing, and handles reporting responsibilities.

However, not all has been smooth sailing. In December 2022, Americor Funding Inc. and Banir Ganatra reached a settlement with the Colorado Attorney General's Office following allegations of improper marketplace conduct. As part of this agreement, Americor committed to adhering to the Uniform Consumer Credit Code and the Debt Management Services Act. Additionally, the company agreed to maintain its registration in Colorado, refrain from enrolling new Colorado consumers for two years, and pay $200,000 in restitution.

Customer Satisfaction

Americor’s improved internal operations have significantly boosted its debt settlement capabilities. CEO David Norris highlighted these advancements, saying:

"Daniel has been an integral part of our executive leadership team and has led the development and expansion of our Negotiations department. As a result of Daniel's leadership, strategic plans, and process improvements, Americor has seen more than a ten-fold increase in our debt settlement production, which has helped catapult both our revenue generation and our brand within the debt relief industry."

This dramatic increase in production underscores the company’s enhanced negotiation strategies and operational efficiency, which directly benefit clients. Combined with its long-standing A+ BBB rating and accreditation, Americor continues to meet client expectations while delivering effective debt resolution services.

Company Comparison: Pros and Cons

Once you’ve examined individual company profiles, comparing key metrics side by side can give you a better sense of how they stack up. To evaluate performance, focus on factors like program duration, fee structures, and settlement success rates - these metrics provide valuable insights into how each company operates.

Here’s what the data reveals: debt settlement programs generally run between two and four years. Clients typically save around 30–50% of their enrolled debt upon settlement, and about 55% of accounts are settled overall. Within 36 months, 74% of clients manage to settle at least one account, 59% settle half of their accounts, 43% settle 75%, and 23% settle all accounts they’ve enrolled.

Fee percentages - usually ranging from 15–25% - are another critical factor to weigh. But don’t just stop at the numbers. Consider how these fees align with customer service quality, program flexibility, and compliance with regulations. Look for signs of proper licensing and strong BBB ratings, as these elements can greatly impact your experience.

Conclusion

When choosing the right debt settlement provider, it’s essential to weigh the factors discussed earlier. Start by confirming the provider’s accreditation with organizations like AFCC, ACDR, or IAPDA. Accreditation ensures adherence to industry standards and ethical practices.

Next, scrutinize the fee structure. Reputable companies should charge 15%–25% of the enrolled debt, and only after successfully settling it. Avoid providers with upfront or hidden fees, as these can be red flags.

Most companies require a minimum of $7,500 in unsecured debt, with program durations typically ranging from 24 to 48 months. Knowing these timelines helps you set realistic goals and better prepare for the financial recovery process.

Look for providers with strong reputations, backed by high ratings on platforms like BBB and Trustpilot. For instance, a 4.7/5 Trustpilot score or recent industry awards are reliable indicators of consistent service quality.

Additionally, consider the range of services offered. Beyond basic debt settlement, some companies provide legal assistance, financial education tools, or even debt consolidation loans. These added services can be invaluable if your financial situation shifts or if settlement turns out not to be the ideal solution.

Platforms like LoanDebtFix.com make comparisons easier by compiling expert reviews, customer feedback, and critical metrics tailored for U.S. consumers.

Finally, remember that debt settlement can affect your credit score and may not be suitable for everyone. Take the time to compare multiple providers, read contracts thoroughly, and ensure the company is authorized to operate in your state. By applying these criteria, you can confidently choose a provider that aligns with your financial goals.

FAQs

What should I look for when choosing a debt settlement company in 2025?

When choosing a debt settlement company in the United States, it's important to pay attention to a few critical aspects like certifications, honesty, and customer feedback. Start by checking if the company is accredited by respected organizations such as the National Foundation for Credit Counseling (NFCC). Also, take a close look at their track record, focusing on success rates and how satisfied their clients have been.

Be sure to review their fees, eligibility criteria, and whether their services align with your financial objectives. A reputable company should be upfront about costs, clearly explain how the process works, and offer strong customer support to help you navigate your debt relief plan.

What are the pros and cons of joining a debt settlement program?

A debt settlement program can be a way to lower the total amount you owe and potentially pay off your debts faster. It also offers an alternative to bankruptcy, which can have lasting effects on your financial future. That said, it’s not without its challenges. Some of the potential drawbacks include a negative impact on your credit score, tax liabilities on the forgiven debt, and the possibility that some creditors might refuse to negotiate. Plus, there’s always the risk of encountering steep fees or even scams if you’re not careful.

Before signing up, take the time to evaluate these pros and cons. Make sure to choose a trustworthy, accredited company to guide you through the process. A clear understanding of the risks and rewards will help you decide if debt settlement aligns with your financial needs.

How does settling a debt impact my credit score, and what can I do to reduce the negative effects?

Settling a debt can negatively affect your credit score because it usually means paying less than the total amount you owe. Creditors often report this as a negative entry on your credit history, and this record can stick around on your credit report for up to seven years. Unfortunately, this can make it harder to qualify for loans or credit during that time.

To soften the blow, you might want to negotiate with creditors to allow partial payments while working through the settlement process. Once the debt is settled, shift your focus to rebuilding your credit. Pay your bills on time every month, keep your credit card balances low, and steer clear of taking on new debt. Over time, these habits can help repair your credit score and improve your overall financial health.